A Strategic Guide to King & Pierce County Foreclosures

The numbers are out, and the headlines are hungry.

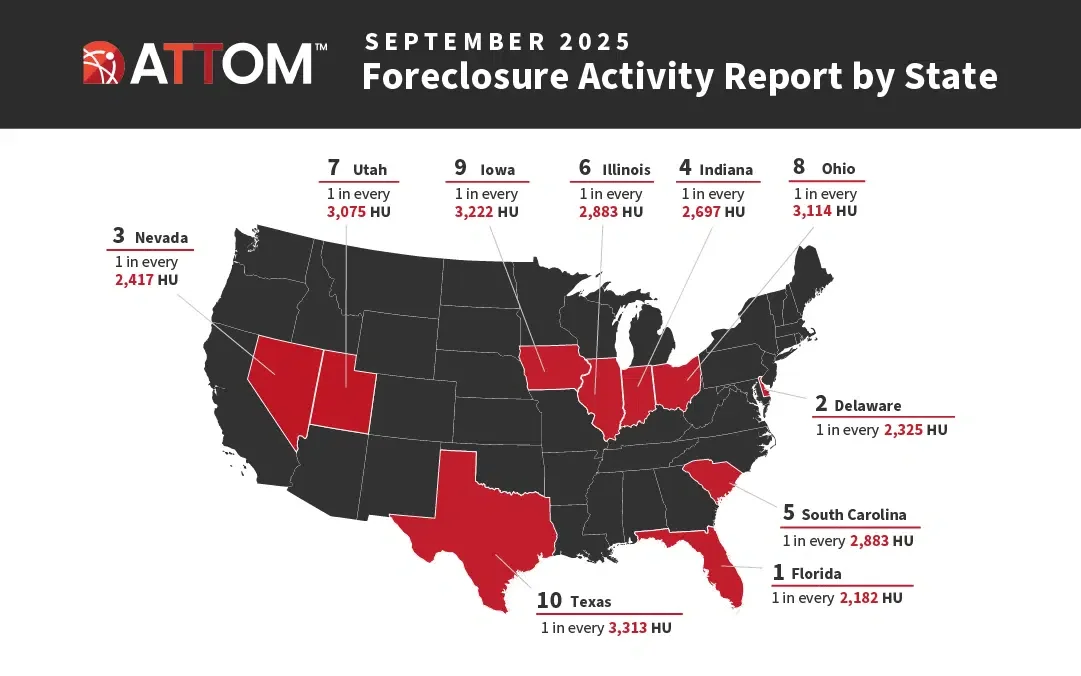

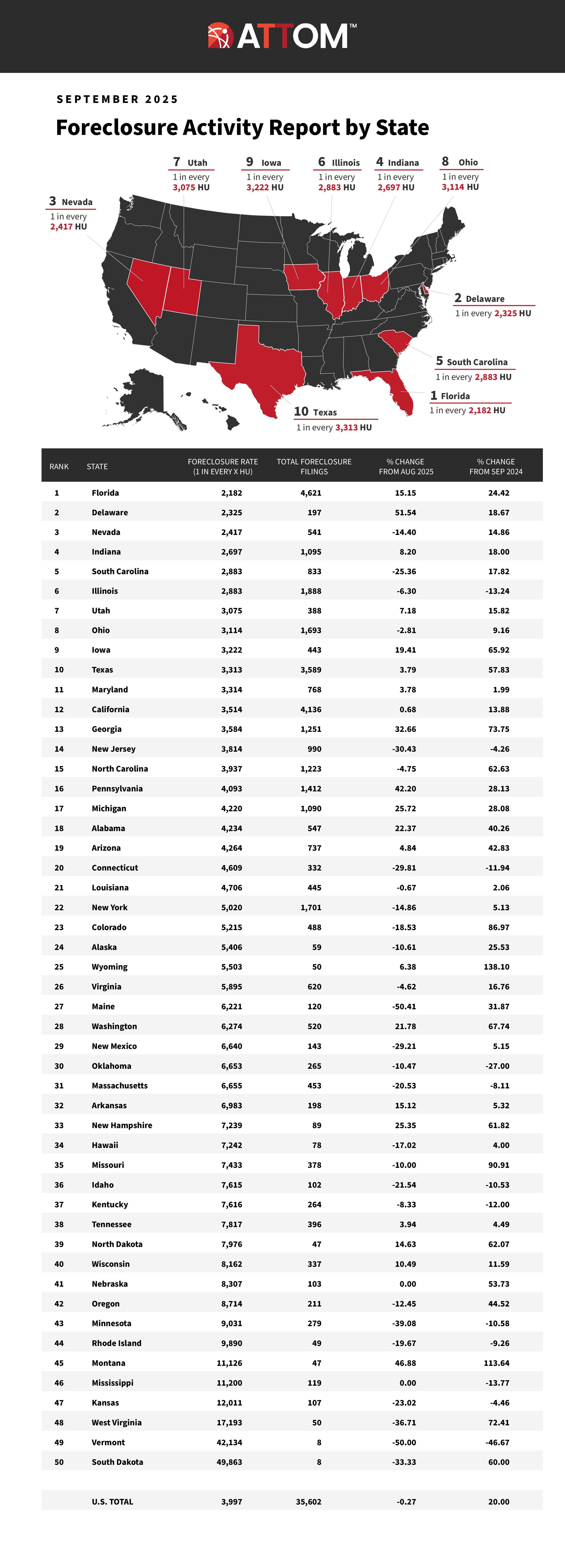

Foreclosure filings in September—35,602 of them, to be exact—jumped 20% from this time last year. Even more telling, bank repossessions (REOs) surged a staggering 44%, according to a recent ATTOM Data Solutions Report

The air is suddenly thick with the smell of opportunity. The amateur investor, high on a diet of home-flipping TV shows, is reading the headlines and seeing one thing: cheap houses.

They are reading the wrong story.

If you're a first-time investor or a savvy homebuyer, let me offer you the first, and most critical, piece of strategic advice: Stop chasing the discount and start managing the risk.

The September spike isn't a 2008-style fire sale. It’s the "Great Normalization." What we're seeing is not a new wave of defaults, but a bureaucratic logjam finally breaking. These are the delayed, lingering effects of expired pandemic-era moratoriums. This isn't a gold rush. It's a complex system moving back to its baseline.

For the strategist, this is an opportunity. For the gambler, it's a trap. This post is your manual for being the former.

Why This National Trend Matters in the Puget Sound

Before you dismiss these numbers, let's bring this home.

While Washington state has a lower foreclosure rate than the national average, the data pinpoints our communities as key areas of activity.

Pierce County: The ATTOM report specifically identifies Pierce County as one of the top three counties in Washington driving this activity. Opportunities are real and present in areas like Tacoma, Puyallup, and Spanaway.

King County: This activity is primarily concentrated in the suburban areas our team has served for decades—communities like Kent, Federal Way, and Auburn.

The opportunities are in our backyard. But so are the traps.

The Investor's Delusion: Why "Cheap" Will Cost You Everything

The biggest mistake a rookie makes is confusing "price" with "cost." A foreclosed home's low price tag is a warning label, not an invitation. You aren't just buying a house; you're buying a black box of unknowns.

The "As-Is" Trap

At an auction, "as-is" doesn't mean "needs paint." It means "the previous owner may have stripped the copper wiring and poured concrete down the drains." You have zero right to an inspection.

The Lien Nightmare

You don't just buy the house; you often buy its debts. The bank's mortgage might be the first lien, but what about the $15,000 in unpaid HOA dues? Or the $8,000 mechanic's lien? They become your problem.

The Auction Gladiator Pit

Let's be blunt. The courthouse steps are not for you. You, with your pre-approval letter, will be standing next to seasoned, all-cash LLCs who buy five homes a week. In the hyper-competitive ring of Pierce and King County, you will not win. And if you do, it's because the pros knew something you didn't.

The Buyer's Playbook: 3 Paths to Buying a Foreclosure

The rookie chases the auction. The strategist knows the real opportunities are found before and after. Here are the three paths.

Path 1: The Empathy Path (Pre-Foreclosure)

This is the most "human" approach. You find the homeowner after they've received a notice of default but before the bank seizes the property.

The Strategy: You are not a vulture; you are an exit ramp. You offer a fair price that helps them avoid a credit-destroying foreclosure.

The Upside: You get to do a full inspection. You get to talk to the owner. You can even negotiate with the bank on a "short sale."

The Catch: It's a slow, emotionally taxing negotiation. But your risk is infinitely lower.

Path 2: The Auction (The Gambler's Path)

This is the courthouse step circus. As we've established, this is not a strategy. It's a gamble. Avoid it.

Path 3: The REO (The Strategist's Path)

This is the path that 44% year-over-year spike is opening up. An REO (Real Estate Owned) is a property that failed to sell at auction and has been repossessed by the bank.

This is your single best entry point.

The Strategy: The bank now owns the house. They are not emotional. They are a corporation with a non-performing asset on their books. They want it gone.

The Upside:

Clean Title: The bank has already cleared other liens to make the property "marketable."

Vacant Property: The bank has handled the (often difficult) eviction process.

It's on the MLS: You can search for these just like a normal house, listed by a real estate agent (<-Click here and sign up to get a search like this)

FINANCING: This is the big one. You can get a mortgage for an REO.

The Pro-Move: How to Finance Your REO Purchase

This is where real expertise matters. The REO path is fantastic, but how you finance it depends on your goal.

For the True Investor (All-Cash or Conventional)

If you're an investor looking to flip or acquire a rental, the REO path is your game. You get all the benefits of a clean title, and you compete on the open market.

Pro-Tip: As an investor, you cannot use an FHA 203(k) loan. However, you can use conventional renovation loans (like Fannie Mae's HomeStyle® loan) which are specifically designed for investors to purchase and repair non-owner-occupied properties.

We can set up a custom REO search for you tomorrow.

For the First-Time Buyer or "House Hacker"

This is the most powerful strategy. You’ve heard of the FHA 203(k) Rehab Loan. It bundles the purchase price and the cost of repairs into a single mortgage. It’s perfect for a beaten-up REO.

Here are the critical nuances:

The Rule: Standard FHA 203(k) loans are strictly for owner-occupants. You must intend to live in the property for at least one year.

The Contractor: The FHA requires all work to be done by licensed and insured contractors. This isn't a DIY-friendly loan; it's a risk-management tool to ensure the property (the bank's collateral) is repaired correctly.

This is a brilliant opportunity for:

First-Time Homebuyers: Find an REO fixer-upper. Use a 203(k) loan to buy it and finance the new kitchen all at once. This is how you build "forced equity."

"House Hackers": The 203(k) can be used on 2-4 unit properties, as long as you live in one. This is a genius path to acquire a multi-family property using a low-down-payment loan.

Are You an Investor or a Gambler?

The September foreclosure data is a Rorschach test. The amateur sees a lottery ticket. The strategist sees a systemic shift.

The strategist ignores the auction, focuses on the REO market, and lines up the correct financing.

This market will punish the unprepared. But with over 70 years of combined experience in these exact neighborhoods, our team [Internal Link: The Scheer Gold Team] knows how to build a winning strategy.

Your first move isn't to look at a single listing. It's to build your plan.

Sources for Further Reading

1. Foreclosure Data & Market Analysis This is the primary source for the September 2025 statistics cited in the article.

ATTOM Data Solutions: U.S. Foreclosure Market Report – September 2025 (Note: This link reflects the source for the data you provided. The exact URL for a September 2025 report would be found on this domain.)

2. Key Terminology & Investor Paths These resources offer clear, third-party definitions of the strategies discussed.

Investopedia: The 6 Phases of a Foreclosure (This guide clearly defines the Pre-foreclosure, Auction, and REO stages.)

Investopedia: What Is Real Estate Owned (REO)? (A detailed explanation of the "REO Path" and why banks sell these properties.)

3. Financing Resources This is the official government resource for the FHA 203(k) loan, the "pro-move" mentioned in the post.

U.S. Department of Housing and Urban Development (HUD): Section 203(k) Rehabilitation Mortgage Insurance (This is the primary source detailing the loan's purpose, types, and eligibility requirements.)